2025 Steamboat Springs Annual Market Report

2025 marked a meaningful shift in the Steamboat Springs real estate market.

What began as a buyer-leaning environment steadily moved toward balance — and by year’s end, the data pointed toward renewed seller strength. While many perceived “more inventory,” active buyers experienced something very different: limited options in the price ranges and property types where demand remained strongest.

Supply was visible — but not abundant.

Pricing held firm. Well-positioned properties sold. And luxury benchmarks were reset.

The Mountain Area tells the story clearly:

37 single-family homes sold

Only 7 active listings at year’s end

Approximately two months of supply

That is seller-side inventory.

Average price per square foot for Mountain Area single-family homes reached a record $940/sf, surpassing Downtown pricing.

Other 2025 highlights:

Downtown/Fish Creek condos & townhomes: record-setting total dollar volume

Mountain Area single-family volume: 20% above the 2021 peak

West Steamboat: record total sales volume

Hayden: new high at $361/sf

And in the luxury segment:

$17,450,000 — highest-priced sale in Steamboat history

$19,675,000 — new record set one month later

Luxury demand remains strong and confident.

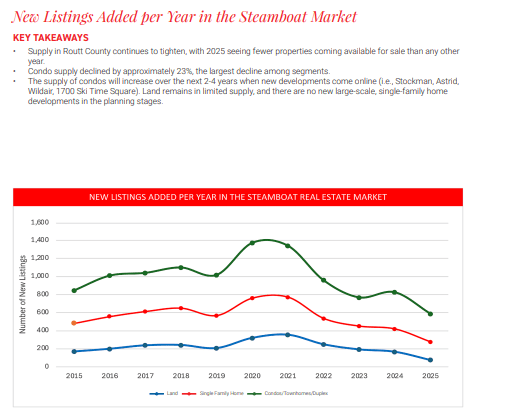

2025 saw fewer new listings added than any prior year.

Condo supply declined approximately 23%.

Land sales dropped significantly across multiple regions.

Transaction counts were slightly lower year-over-year — but total dollar volume remained flat.

This indicates pricing strength rather than contraction.

The market did not correct broadly. Instead, it recalibrated.

One defining theme of 2025 was the divergence between Steamboat’s core resort areas and surrounding communities.

Primary resort neighborhoods showed resilience across pricing and absorption.

Some feeder markets experienced slower volume and more pricing sensitivity.

Limited inventory and small transaction counts amplify year-over-year swings — especially in areas like Stagecoach, Hayden, and Oak Creek.

For strategic buyers, these shifts may represent opportunity.

Three major base-area projects are expected to break ground:

The Stockman

Wildair

1700 Ski Time Square

Approximately 150 new residences are projected, with early pricing indications around $2,500 per square foot, and upper-tier offerings approaching $4,000 per square foot.

Historically, high-end slope-side development places upward pressure on pricing across the broader region as buyers expand their search beyond the base area.

2026 will likely be defined by development-driven momentum.

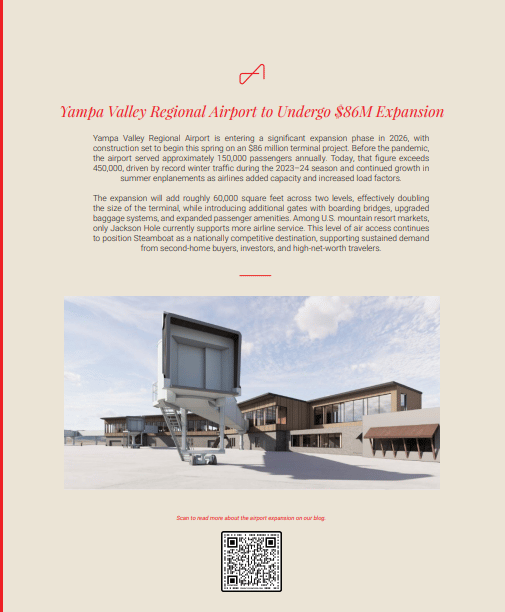

The Yampa Valley Regional Airport will begin construction on an $86 million expansion in 2026, nearly doubling terminal capacity.

Passenger traffic has grown from approximately 150,000 annually pre-pandemic to over 450,000 today.

Among U.S. mountain resort markets, only Jackson Hole supports more airline service.

This level of air access reinforces Steamboat’s position as a nationally competitive luxury destination — supporting sustained demand from second-home buyers and investors.

Compared to Aspen, Telluride, Beaver Creek, and Snowmass, Steamboat remains relatively attainable on a price-per-square-foot basis while demonstrating upward pricing momentum.

Steamboat continues to offer a compelling value proposition within the Colorado luxury resort market.

Inventory remains constrained.

Pricing has proven resilient.

New development and infrastructure investments are underway.

The market feels less like a correction — and more like a coiled spring.

In the full report, you’ll find:

Detailed regional breakdowns

Market comparison tables

Notable sales

Development insights

Commercial market data

Forward-looking analysis

Button

Luxury Real Estate

South Routt County estate with mountain views, equestrian potential, and room to roam near Steamboat Springs

Whether you are looking to buy or sell in Steamboat, she hopes that you will allow her to work for you. Contact her now!